Research

Trends in Reverse Mortgages - A New Option For Senior Homeowners

Everyone’s needs are unique--but a desire to enjoy a full life is universal. Often, this means having enough money to cover bills and relieve some of the anxiety that comes from figuring out how to make retirement more comfortable.

Many retirees looking for ways to supplement fixed incomes and defray living expenses are increasingly finding the answer in their homes--it is called a reverse mortgage.

The versatility of reverse mortgages has already been demonstrated by thousands of seniors who have used this tool to help them generate the cash needed to assist with a wide variety of financial needs. These loans, designed to give senior homeowners access to the wealth in their homes, have helped seniors remain in their homes, fund home health care, pay for modifications which made their homes safer, or simply created an income stream that provided seniors with peace of mind.

While still only a narrow slice of the home loan market, the reverse mortgage as a product is gaining at just the right time demographically. Increasing numbers of seniors have significant equity in their homes, but little in the way of income with which to meet increasing expenses, particularly in the area of health care, and many seniors simply don’t want to leave the home they’ve made for themselves. The "graying" of the baby boom generation clearly signals that the seniors of the near future will not only be more active in general, but will likely remain active for many more years than previous generations.

Industry Trends

The mortgage industry forsees a strong growth ahead for reverse mortgages amid a demographic shift to senior citizens as “Baby Boomers” approach retirement age. According to Fannie Mae, currently 20 million+ people are older than 65. Of these, 77 percent are homeowners and 84 percent own their home free and clear. Best of all 85 percent of senior homeowners want to remain in their home according to an AARP (American Association of Retired Persons) study.

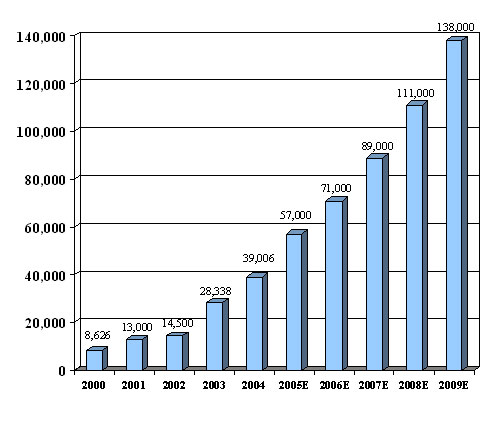

Just a few years ago reverse mortgages weren’t on most consumers’ radar screens. But as the industry has educated consumers about these unique loans, their popularity has grown tremendously in a short time. The number of people taking out reverse mortgages has soared over the last five years, climbing from a loan volume of fewer than 6,000 loans annually prior to fiscal year 2000, to over 48,000 just in 2005, according to the U.S. Department of Housing and Urban Development (HUD).

This year, the industry is on pace to help even more seniors live a more comfortable lifestyle.

The Reverse Mortgage Forecast

* Source: HUD Data as provided by MBA of America

According to the U.S. Census, the population of seniors age 65 years and above is projected to increase 147 percent between 2000 and 2050. Currently seniors own over $2 trillion in home equity (NRMLA) and less than 1 percent has been tapped by the reverse mortgage program.

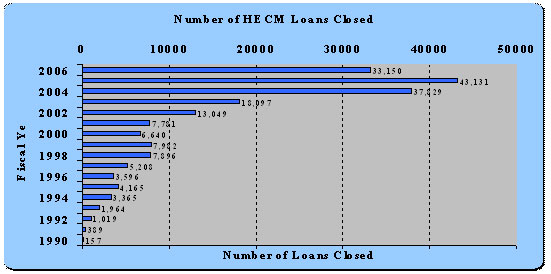

Below is an illustration of the number of Home Equity Conversion Mortgage (“HECM”), the House and Urban Development reverse mortgage program, loans funded nationwide from 1990 to March of 2006, demonstrating the expansive market in the reverse mortgage industry.

(Number of HECM loans closed nationwide: Fiscal Year ending October 1 – September 30 of following year.)

* Source: HUD – FHA

Expanding Use of Reverse Mortgages

Reverse mortgage loans are not appropriate for everyone. However, anecdotal evidence suggests that seniors of all income levels are cashing in on their home by using reverse mortgages for many different reasons. For many older homeowners, reverse mortgages provide the extra dollars that let them stay securely in their homes throughout retirement, help pay for home repairs and improvements, give gifts to their children and grandchildren or to continue their education.

For others, the funds from a reverse mortgage are being used to pay taxes, support health care needs such as prescription drugs and medical care, including care at home or in funding long term care expenses.

And for a growing group of seniors, reverse mortgages provide a means to live more comfortably and pursue their dreams. For example, the funds have been used to buy everything from a second car, an airplane or recreational vehicle, or taking a dream vacation.

Reverse Mortgages Explained

A reverse mortgage enables homeowners aged 62 or older to convert part of the equity in their home into income without having to sell the home, give up title, or take on a new monthly mortgage payment. Borrowers will never, under any circumstances resulting from the reverse mortgage, be forced to leave their homes providing they make their real estate property tax, insurance payments, and maintain the property in a reasonable condition.

Borrowers can choose to receive the reverse mortgage funds as a lump sum, monthly income (for up to life in the home), a line of credit, or any combination. Borrowers make no monthly mortgage payments on a reverse mortgage during the life of the loan. The loan becomes repayable when the borrower sells the home or permanently moves out (vacates the home for 12 consecutive months). In addition, the repayment amount can't exceed the value of the home at the time of sale. Most important--the funds from the reverse mortgage are tax-free** and can be used for any purpose.

The most popular reverse mortgage is the Home Equity Conversion Mortgage (HECM), which is insured by the Federal Housing Administration, an arm of the U.S. Department of Housing and Urban Development (HUD). For higher value homes (the jumbo market) Financial Freedom Senior Funding Corporation offers a proprietary loan called the Cash Account Advantage. These loans offer a variety of fee structures with loan options which have no up front fees for the borrower. Fannie Mae offers the HomeKeeper loan.

All three reverse mortgage products have numerous built-in consumer protection features, so borrowers can be confident about their decision. Mandatory third-party HUD-approved counseling, rate caps on all products, comprehensive disclosures, and retaining title to the home are consumer protections built into these products, just to name a few. Deciding to take out a reverse mortgage is a choice that should be considered carefully since the house is often a family’s most valuable financial resource.